A household explores career options.

The Facts

Married couple, Age: 40

Sandy's earnings: $60,000

Erin's earnings:$120,000

Erin's employer 401(k) contributions: $10,000

Retirement Assets: $400,000

Regular assets: $100,000

Housing: $500,000 home w/ $250,000 mortgage

Current discretionary spending: $65,000

Sandy and Erin are mid-career professionals with a 12-year old daughter. Sandy is very happy with her career as a social worker, while Erin is burnt out from her corporate job. They both want to retire at 65 and send their daughter to college. Their big question – can they afford for Erin to change to a less remunerative, but more satisfying career? In particular, what will it mean for their sustainable living standard?

Erin would like to transition into education. But doing so entails a major pay cut. She has several job offers and is weighing her options. The position she likes most comes with sticker shock. It only pays $80,000 a year and there is no employer 401K contribution. Erin’s worried that switching careers would come at a huge cost to her family’s living standard. To see what’s involved, Erin and Sandy model their current situation as their “Base Plan” in MaxiFi and set up an alternative profile, “Career Downsize,” which specifies Erin’s career switch.

The Base Plan

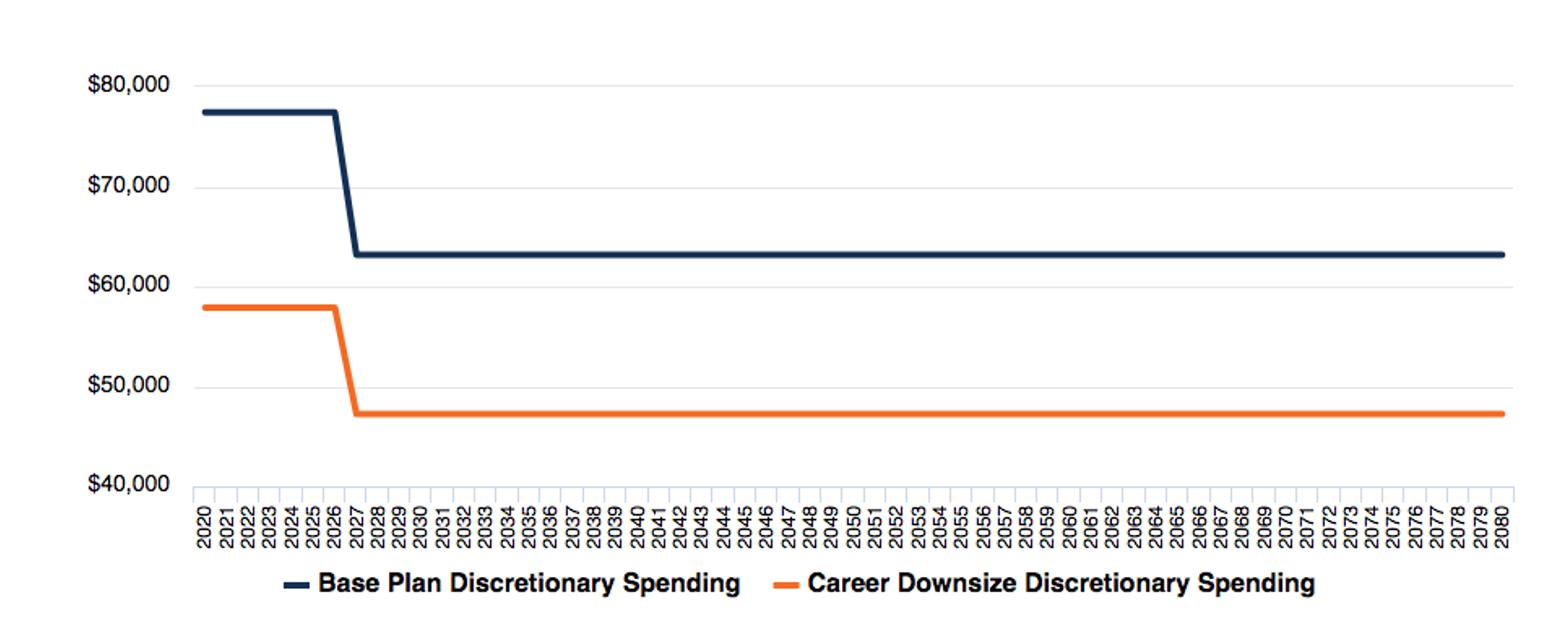

According to their Base Plan, Sandy and Erin can spend $77,444 per year on a discretionary basis while their daughter is at home, with a reduction when she goes off to college reflecting the fact that one fewer mouth needs to be fed. Discretionary spending is all expenditures apart from fixed (off-the-top) outlays on taxes, housing, insurance, retirement contributions and special expenses, in this case college for their daughter. Since the household is never borrowing constrained, their living standard per equivalent adult always stays fixed.

The good news is that the couple’s actual current discretionary spending is $65,000 a year. Hence, they are spending within their means according to the Base Plan.

The ‘Career Downsize’ Plan

Under the alternative plan, Sandy and Erin’s discretionary spending drops to $57,899 while their daughter is living at home (see orange line below). This is nearly $20,000 less than under the Base Plan (see blue line below). Importantly, it’s also less than the their actual $65,000 in current discretionary outlays. Hence, Erin’s immediate career switch is unaffordable unless Sandy and Erin make other adjustments to their plan.

The ‘Delay Career Downsize’ Plan

To make the career switch work, Sandy and Erin make some adjustments.

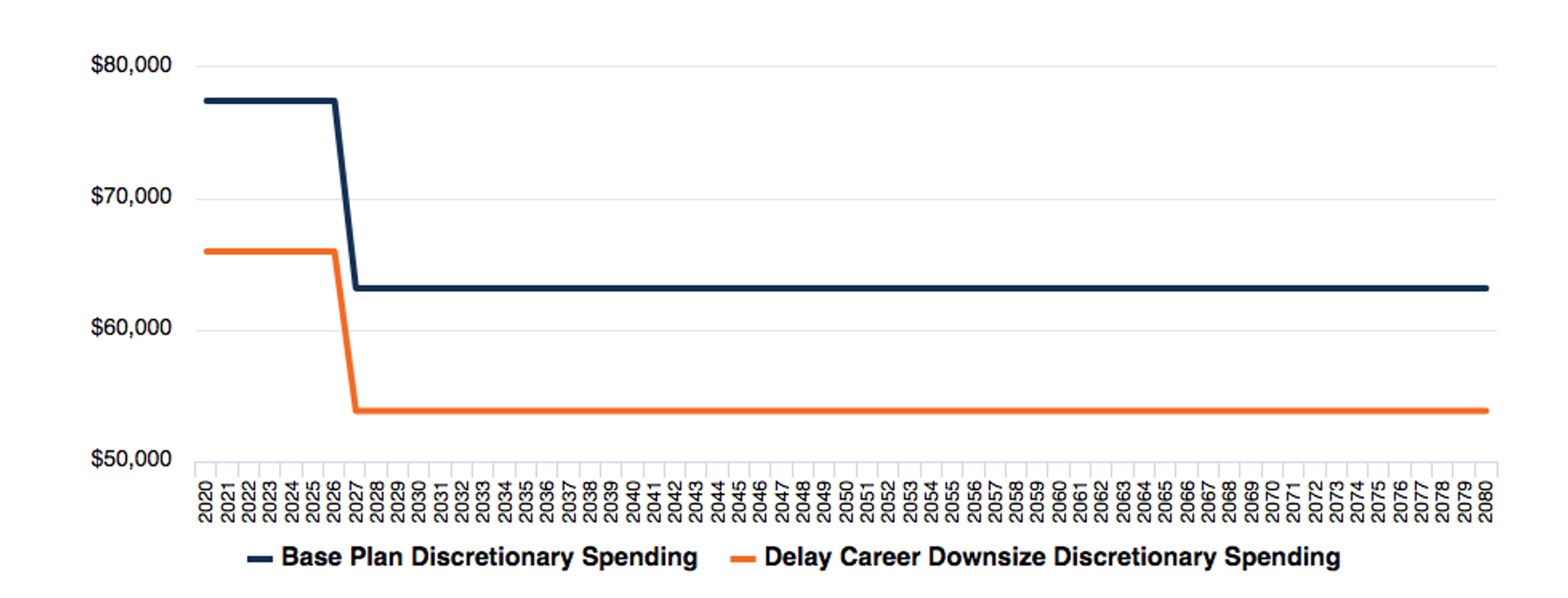

First, Erin agrees to stay in her current job for another 4 years. This generates an additional $160,000 in salary plus $40,000 in employer 401K contributions over the next four years. Second, Sandy commits to taking on a few more clients, which she’s been considering anyway. This will increase her annual compensation to $70,000 from $60,000.

Sandy and Erin set up a second alternative profile, “Delay Career Downsize,” to consider these adjustments. Now their pre-college annual discretionary spending is $65,980 (see orange line below), which is affordable since it’s more, if only slightly, than the $65,000 they are currently spending. In short, making these changes lets Sandy and Erin have their cake and eat it to.

Conclusion

MaxiFi is a great tool for exploring alternative careers/jobs. Many of us feel financially locked into work positions we hate. But switching to less remunerative, but more satisfying work may be more affordable than it seems. First, our taxes will be lower. Second, we may be able to work longer if we like what we’re doing. Third, we may be able to make other adjustments, including downsizing our homes or moving to a cheaper state (e.g., one without an income tax), or making adjustments like those chosen by Sandy and Erin.

Contributed by

Jay Abolofia, PhD, CFP®

Lyon Financial Planning | Founder

781-218-9005