A household explores the benefits of consumption smoothing.

The Facts

Married couple, Age: 55

John's earnings: $80,000

Mary's earnings: $80,000

John's 401K savings: $300,000

Mary's 401K savings: $300,000

Non-retirement assets: $150,000

John and Mary, like all of us, want to maintain our living standard through time. Economists call this consumption smoothing. It reflects human nature. No one wants to splurge today and starve tomorrow or vice versa. To help John and Mary achieve a smooth living standard, MaxiFi determines the annual discretionary spending their household can afford and leave all household members with each the same living standard through time. It also calculates the life insurance needed to ensure that survivors have the same living standard or better than it would experience were no one to die.

The Base Plan

Discretionary Spending is Smooth -- the Benchmark Case

Data for John and Mary, a hypothetical couple, are shown above. Although it's not shown, we've also entered a Social Security earnings history for each spouse.

After running the Base Plan, we see that John and Mary's annual discretionary spending is $83,063. Discretionary spending is all outlays apart from fixed (required) expenditures on taxes, housing, Medicare Part B premiums, and special expenses.

The What-If Plan

An illustration of dynamic programming at work and consumption smoothing

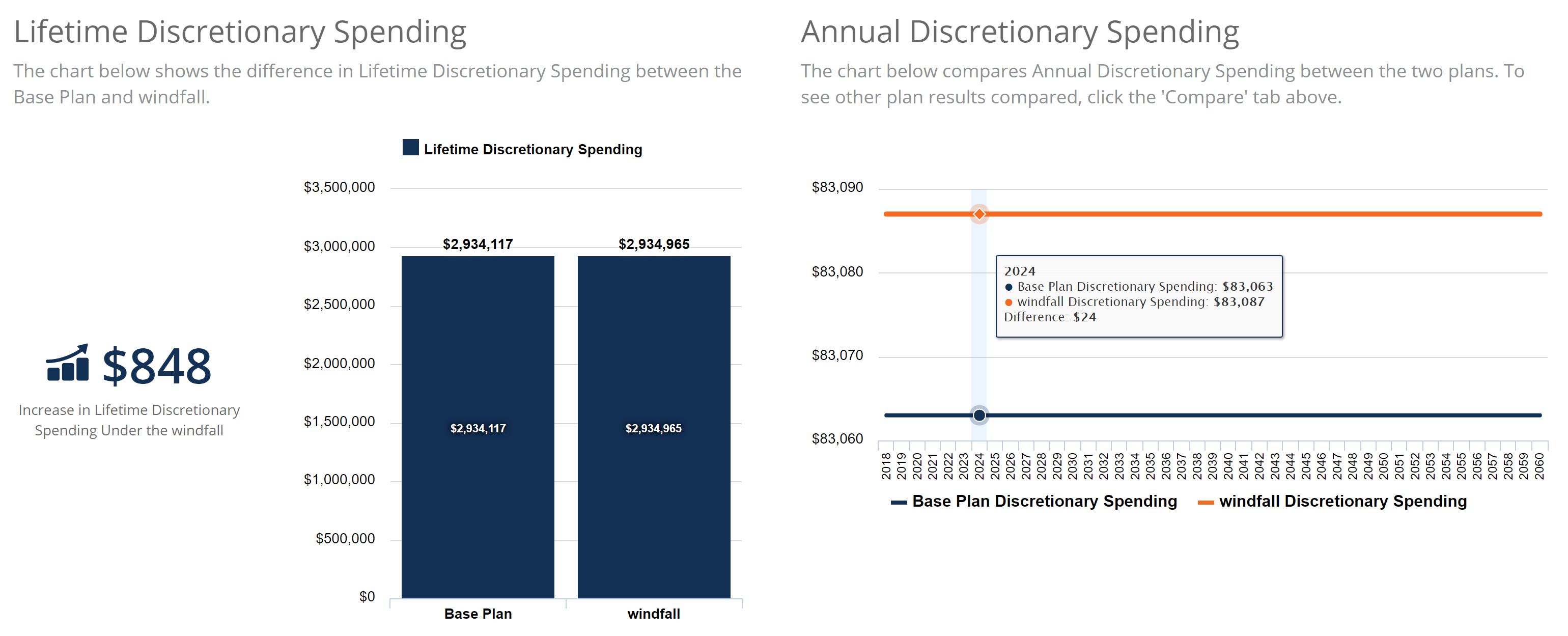

Let's imagine now that John and Mary have some future windfall coming their way. Let's begin with a simple example, just to show how this works, where they learn that they will receive $1,000 five years from now. With the $1,000 programmed into the model, they now have a discretionary spending of $83,087.

Let's study this chart above for a moment.

The graphic at the right reveals that the impact of a $1,000 windfall does not come all at once, raising their discretionary spending five years from now. Instead, this windfall is anticipated in the current year and smoothed in advance providing a new discretionary spending that is $24 higher each year. The lifetime value, given the time-weighted value of money or "present value" is $848. Let's repeat because it's important: Even though the $1,000 is anticipated 5 years from now, if we plan for it we can take advantage of it in the current year. We see how it impacts every year from now until the end.

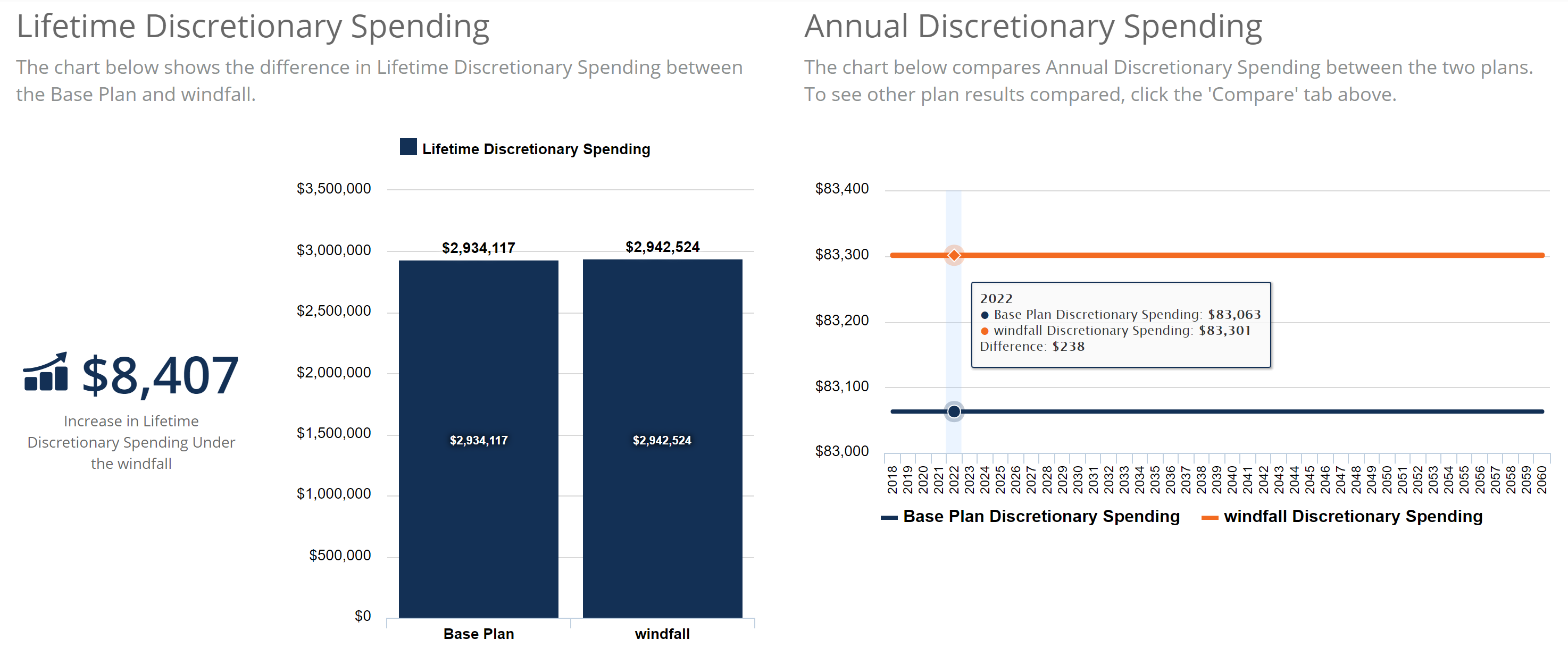

And what if the windfall is $10,000 instead of $1,000? The chart below shows this new $238 annual difference.

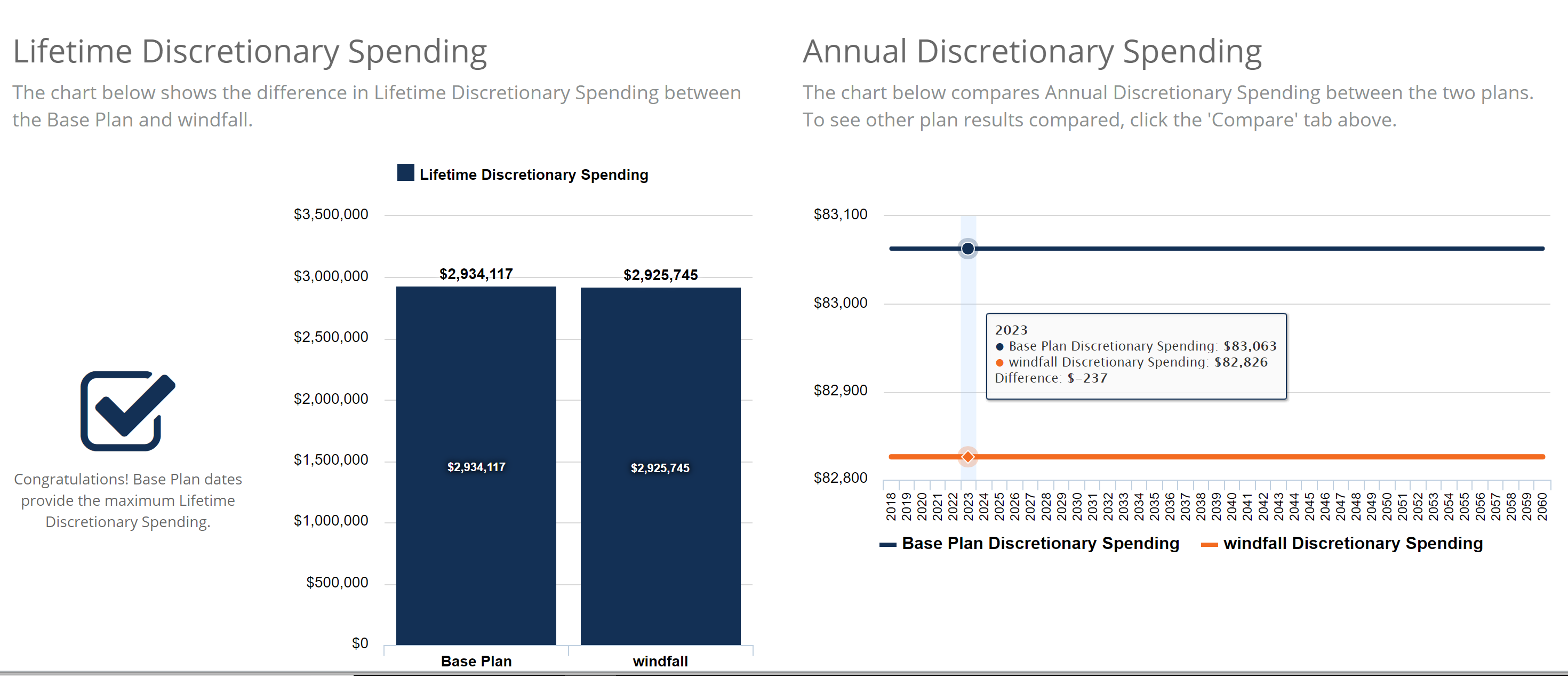

And what if the $10,000 is not a receipt but rather an expense? The chart below shows the difference that a future expense, as opposed to receipt, of that amount would make compared to the Base Plan. In this chart the orange line is now on the bottom. The $10,000 expense does not change the discretionary spending in that year, but rather we see that this expense is anticipated dynamically and discretionary spending is smooth, but at a lower level, from the current year through to the couple's maximum ages of life -- 100.

How Does this Plan Work?

Dynamic programming and the consumption smoothing––the smooth discretionary spending that results--is at the heart of MaxiFi Planner. When you understand this concept, you can begin to imagine many powerful ways to put the program to work. We've seen above that an expense or a receipt at any time in the future is anticipated or taken account of in the current year through to the end of the model.

Downsizing your home in the future is effectively equivalent to adding a special receipt, but one that's far larger than our $1,000 example. Changing to a more expensive home is effectively like incurring an special expense. College expenses, special vacations, expensive weddings, an inheritance, the sale of a business, the purchase of a new car, selling the yacht . . . these examples all work in the planning model just like we illustrated with the $1,000 example above.

Keep in mind as well that a future special expense or receipt might also come as an annual series. So paying off a loan or receiving payments on a loan work just like a single expense or receipt: the impact on spending this year and beyond is calculated dynamically. When you build a planning model that changes the way you collect Social Security benefits--say replace one series of lifetime payments beginning at full retirement age with another, higher, series of payments beginning at age 70––you are essentially exploring the impact of the effect on discretionary spending from the current year through to the end.

Expenses or receipts can be entered so that they are subject to the appropriate tax consequences or simply non-taxable. MaxiFi Planner knows the tax consequences of Social Security benefits. Learn more about Postponing your Social Security Benefits.

The Economics Approach In Action

No financial decision stands alone: income affects taxes, taxes affect spending, Social Security benefits and retirement account withdrawals affect income, which affects taxes, and on and on. Because MaxiFI Planner accounts for all of these mutual influences, it provides an accurate and sophisticated approach to financial planning that you can't find in other planning calculators. Even a $1,000 expense far into the future impacts what we can spend this year. No other calculator does this kind of dynamic programming. Because you can see the impact of all of your lifetime expenses and receipts in terms of available discretionary spending, an annual amount that is recalculated with each new model you build, you can quickly compare models in ways that have practical and intuitive meaning.