A couple explores the option of getting an advanced nursing degree.

The Facts

Married couple, Husband's Age: 38; Wife's age: 28

Toby's earnings: $80,000

Gina's earnings: $50,000

Toby's 401K savings: $50,000

Gina's 401K savings: $10,000

Toby's Employer Contributions: $10,000 (when working)

Gina's Employer Contributions: $5,000 (when working)

Toby and Gina want to understand the impact on their finances—current and future—if Gina were to pursue an advanced degree in Nursing for 3 years. She could double her salary from $50,000 to $100,000 according to the Bureau of Labor Statistics. This suggests a living standard improvement in the long run. However, the downside needs to be evaluated. The degree requires $60,000 in loans and a reduction in her current salary to half time for three years. Likewise, the overall cash constraint on their living standard remains unclear.

The Base Plan

Gina sticks with her current nursing job

Toby and Gina create a Base Plan. This enables them to test a scenario where Gina continues working for $50,000 wit standard cost of living adjustments to her salary each year.

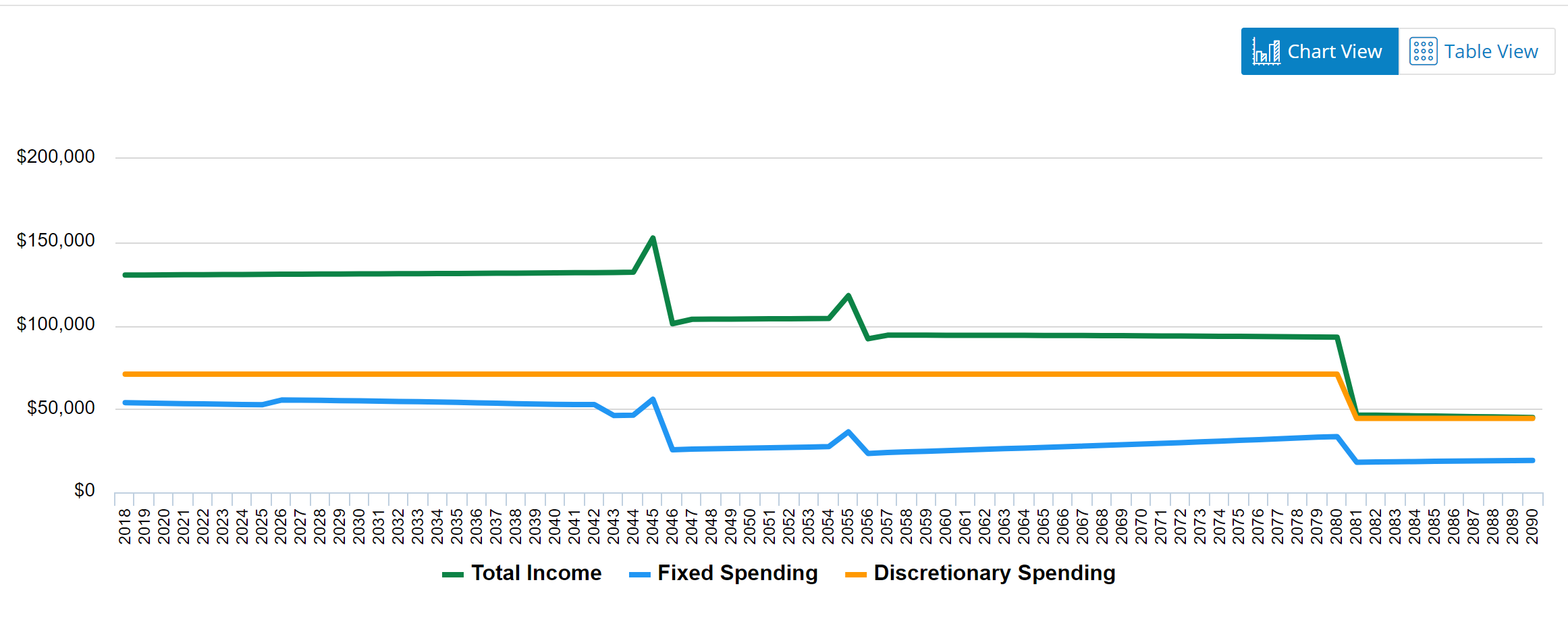

Their Base Plan results in $72,080 in annual discretionary spending from now to retirement. Discretionary spending is the amount left over to spend each year after paying fixed expenses: taxes, housing costs, and Medicare Plan B costs (in their retirement years).

The discretionary spending amount is in "today's dollars," which means it's adjusted for inflation each year and it remains steady (there is no cash constraint or children in the home) even though income and fixed spending changes a lot.

The What-If Plan

Gina pursues an advanced degree to become a nurse practitioner

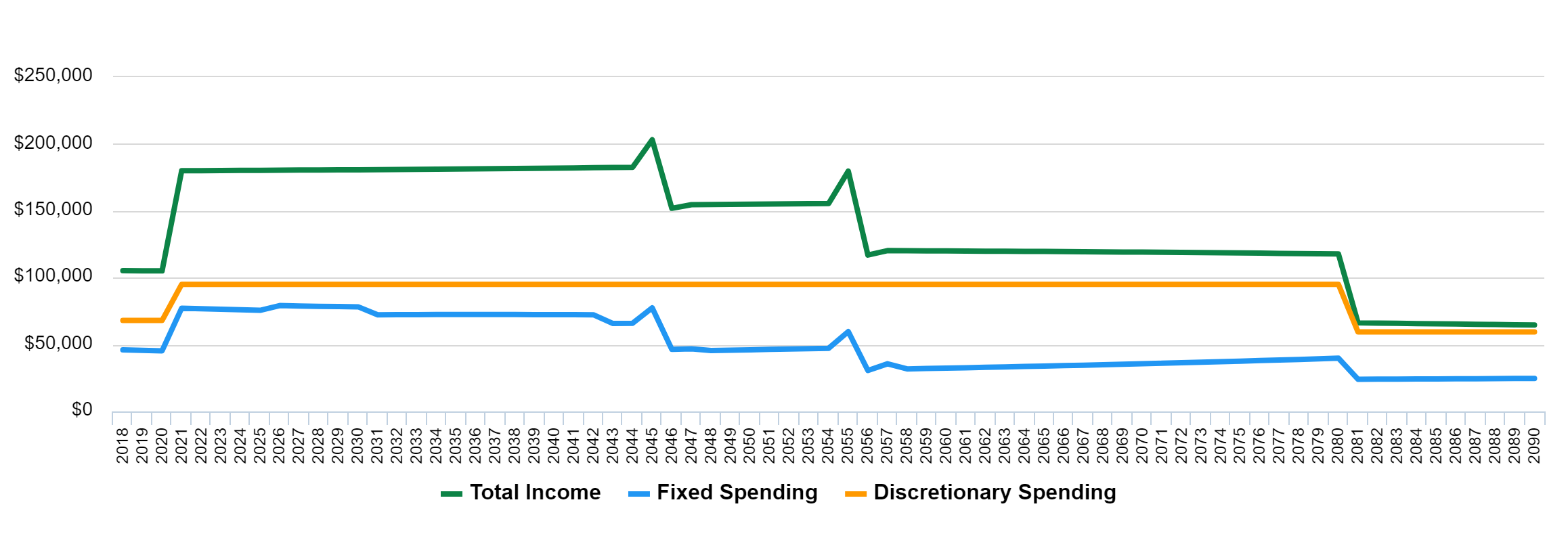

Toby and Gina then create a what-if scenario where Gina works part time for three years at half-salary and takes a new $100,000 salaried job in the 4th year. This plan results in a smooth discretionary spending level of $95,749 - far higher than $72,765 produced in their Base Plan.

A number of realistic adjustments must be made to model this plan correctly. Gina's employer contributes 10% of her salary to her retirement plan. These contributions are reduced from $5,000 to $2,500 for the period of three years while she's in school. After that, the contributions go up to $10,000 per year.

The cost of the Advanced Nursing program is $60,000. The repayment of this loan at 6% interest - beginning when she gets her new job - requires annual payments in nominal dollars of $7,421 annually for ten years.

How Does this Plan Work?

There are a number of factors in combination which result in a $22,984 annual raise in discretionary spending. Although there is a three-year, 50% cut in Gina's salary, and a $60,000 school loan to pay off, the increased salary over her lifetime supersedes these costs. Gina's employer retirement contributions are cut in the short term. But they increase significantly once she earns her new salary. Her Social Security benefit at her "full age of retirement" goes up from $26,198 to $40,375. Her retirement assets under the "advanced degree plan" accumulate to $562,705 in today's dollars the year before she retires. These assets would have been $320,006 if they elected the base plan.

(with the cash constraint)

The Bottom Line

The benefits of this strategy are obvious. If Gina succeeds in school and if the improved job comes through, the decision is worthwhile. Through the power of the dynamic programming in MaxiFi, they can make an informed decision regarding future earnings even in the current year. This is due, in large part, to the $150,000 in regular assets they would employ to bridge the gap until the new, higher salary begin. Again, the advantage is a lifetime discretionary spending of $95,749 compared to the base case of $72,080.

But what if they did not have this $150,000 in cash reserves but instead only $25,000?

In that case, their Base Plan would provide them a smooth $70,857 in discretionary spending, but their What If plan would take on some cash constraint. Specifically, in the What If plan, assuming their cash reserves were $25,000 instead of $150,000, they would experience a discretionary spending level of $68,033 for the first three years and then $95,046 for each year after. Even in this cash-constrained scenario, the three-year period where their discretionary spending is reduced by $2,824 a year is worthwhile in the longterm. The power of MaxiFi allows Toby and Gina to explore these and many other variations on this scenario.

But most importantly, the user is not comparing "theories" or "rules of thumb." MaxiFi provides accurate numbers to compare the real, annual impact on your living standard in order to understand certain household economic decisions like financial planning for education.