Life Insurance Needs Change Through Time

The Facts

Married, Age: 32, no children

Husband Earnings: $90,000

Wife's Earnings (part time): $30,000

401K savings: $50,000

401K contributions: $8,000 including employer match

Life insurance comes in two basis varieties -- term and whole or universal life. Term insurance is straitforward. If you die, your survivors receive the agreed amount. Universal life or whole life insurance policies combine term insurance with saving plans. These policies are often quite complicated. Many seem designed to help the insurance company more than the customer. MaxiFi recommends term insurance to ensure that survivors are able to maintain the same living standard as they would have enjoyed had no one passed away.

Living standard references MaxiFi's suggested level of discretionary spending per household member with adjustments for economies in shared living and the fact that children are generally less expensive than adults. Discretionary spending, in turn, is the household's outlays apart from its fixed spending on housing, taxes, Medicare Part B premiums, college support, alimony, and all other off-the-top expenses. MaxiFi finds the path of annual discretionary spending that maintains the household's living standard through time subject to the household not going into debt or going deeper into debt. I.e., the program's spending recommendations accommodate the household's annual cashflow constraints.

In making its life insurance recommendations, MaxiFi recognizes that the household will now have one fewer mouth to feed and, therefore, doesn't need to as much discretionary spending in the future to maintain its prior per-member living standard. But when a household member passes, MaxiFi also realizes that there are smaller economies in shared living for the household to enjoy due to the reduced number of people in the household.

Life insurance is needed on a household head or spouse/partner if that person's death will reduce the household's future income by more than it reduces the household's future spending. Hence, as a household member reaches retirement, the person's future income declines much more rapidly than the person's future spending (if she/he survives). Consequently, the need for life insurance declines. At some point there is no need for life insurance. This occurs when survivors would actually enjoy a higher living standard after the potential decedent dies than were he/she to remain alive. In this case and at that point, MaxiFi recommends no life insurance holdings on the life of that potential decedent.

The Base Plan

Insurance needs

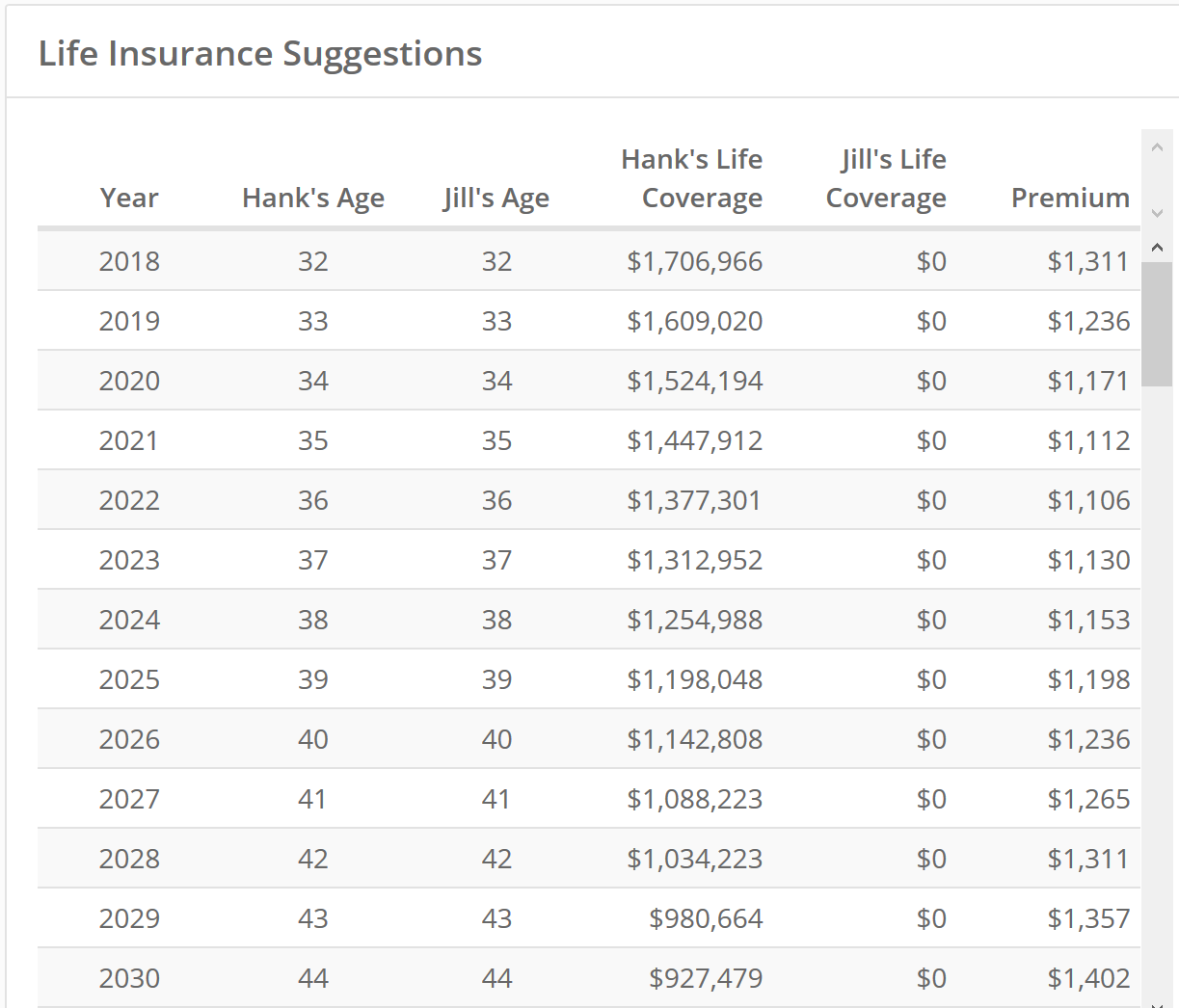

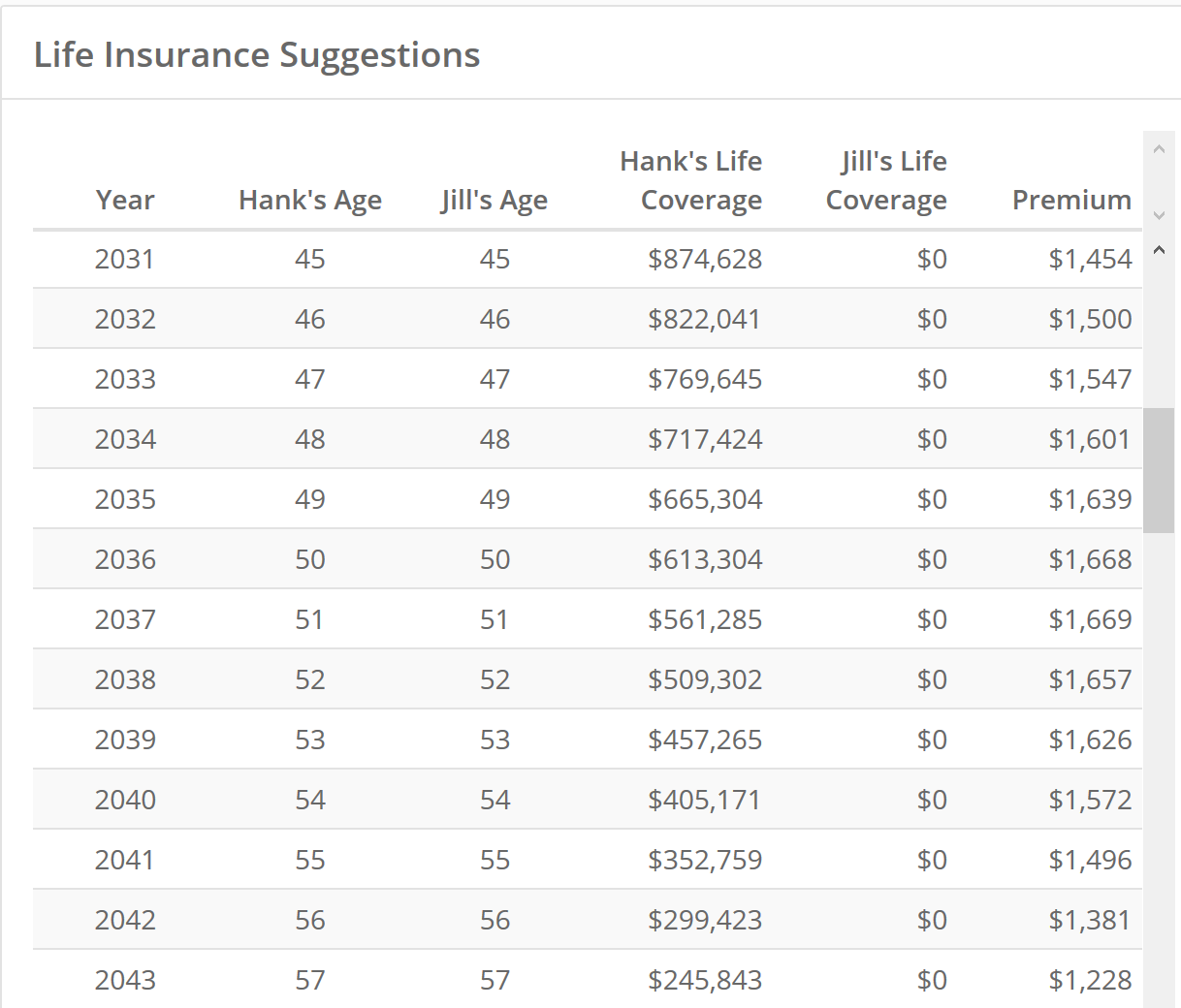

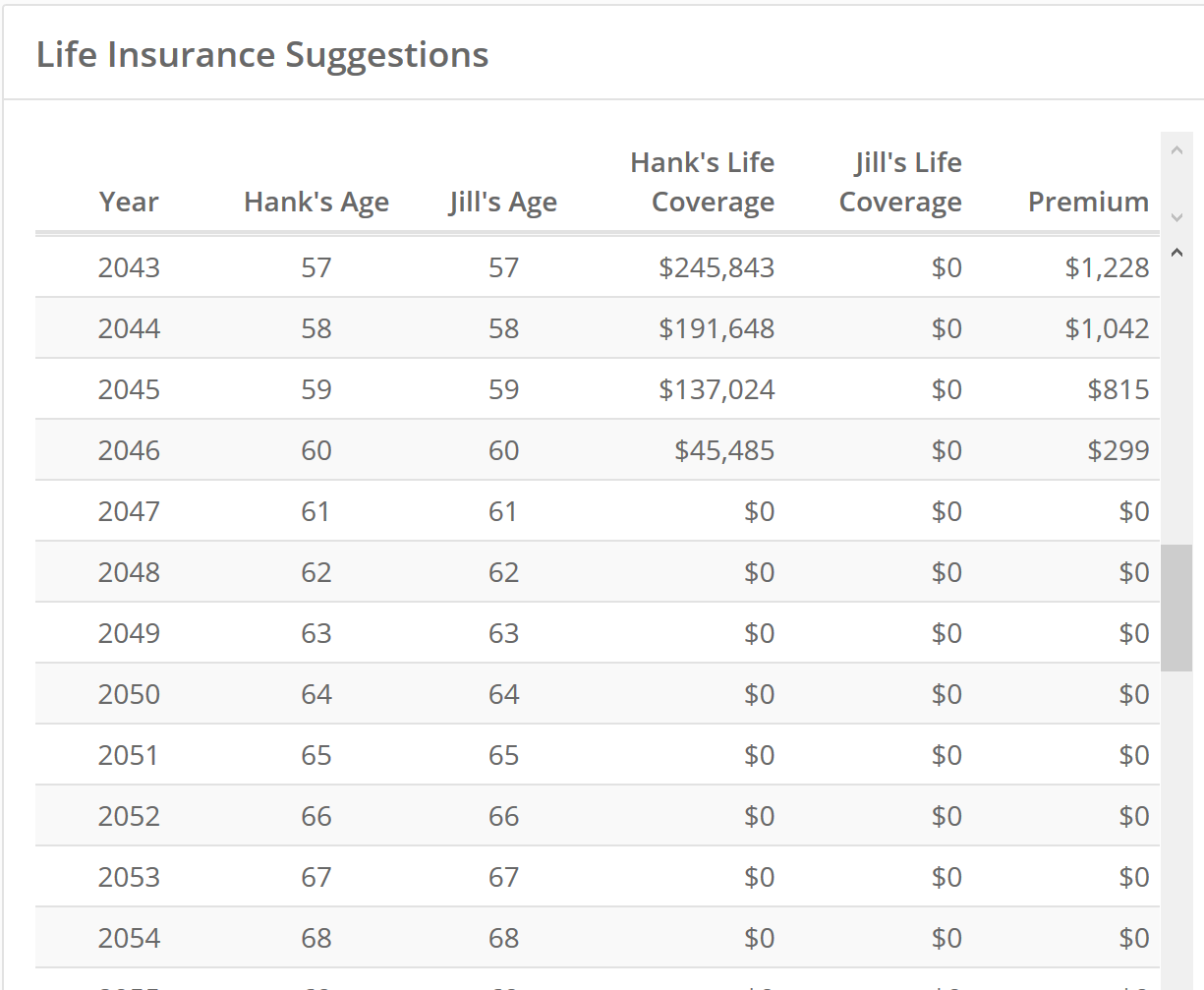

Consider a married couple, Hank and Jill, whose basic data are listed above. MaxiFi shows Hank needing $1,706,966 in term insurance in the current year. In each year thereafter Hank's recommended annual term life insurance holdings decline. Once he reaches at 61, Hank needs no life insurance whatsoever to assure Jill the same life style were he to pass. At that point, he has all his labor earnings behind him. Should he die, Jill would have a higher living standard than had Hank continued to live.

When both spouses are alive, MaxiFi planner recommends $53,736 per year (adjusted for inflation) in discretionary spending. Since the program assumes that 2 can live as cheaply as 1.6, $53,736 per year in discretionary spending translates into $53,736 divided by 1.6, producing a living standard of $33,585. If Hank dies before age 61, having purchased MaxiFi's recommended amount of life insurance, Jill will have enough resources to spend, on a discretionary basis, precisely $33,585 per year. If Hank dies after reaching age 61, Jill will be able to spend more than $33,585 even though Hank holds what the program recommends -- zero life insurance.

In making Hank's life insurance recommendations, MaxiFi considers the case of greatest need, namely that Jill dies at her maximum age of life. It also takes into account that Jill's future taxes and Social Security benefits will change depending on Hank's exact date of death. These and other factors make calculating life insurance needs extraordinarily complex.

The table shows (in today's dollars) MaxiFi's Annual Recommended Levels of Term Life Insurance on Hank's Life.

Over time, recommended term insurance declines. Once Jill's living standard would exceed their current life insurance were Hank to pass away no insurance is recommended. MaxiFi shows not just suggested life insurance holdings but also estimated annual life insurance premiums. The program permits you to specify higher or lower insurance premium rates than the program's default values.

To comport with MaxiFi's suggestions, Hank and Jill can purchase policies with declining term insurance of buy overlapping multiple policies and let some elapse through time. Insurance companies can help tailor one's holdings to MaxiFi's recommendations. But be wary of policies that are complicated. Complicated is generally a cover for consumer fraud.

The Bottom Line

Calculating how much life insurance you need is complicated business. The goal should be to permit your survivors to maintain their current living standard into the future. MaxiFi does this. The program shows that as people age, the amount of life insurance needed to protect survivors declines. Of course, we typically don't buy one-year term life insurance. But one can purchase multi-year, annual renewable term policies to comply, at least roughly, with MaxiFi's suggestions.