A Couple Asks How Much Do We Need to Retire?

The Facts

Married couple: Age: 58

Eve's earnings: $90,00

Owen's earnings: $90,000

Eve's pension: $18,000

3.5% nominal return on non-retirement assets

4.25% nominal return on retirement assets

Combined 401K savings: $500,000

Regular savings: $100,000

Housing: Own $350,000 home

Combined cost of health insurance

continuation til age 65: $7560.

Eve and Owen are finally starting to get serious about retirement planning. They have saved reasonably well but they worry it's not enough. It has helped that their employer contributes annually to their pool of retirement assets. They have been reading a lot of financial news sites with personal finance and retirement columns that make claims like the following: "You need at least one million dollars to retire." (or two million or five million, etc.) Others talk about a special "number" that is needed. Eve and Owen wonder if their combined total of $500,000 in their 401K is enough. Eve and Owen learn that the answer to this question is not so difficult to discover or so vague as these rules of thumb about a "number" led them to believe. They set up their current case in MaxiFI Planner to create a base plan. They also set up a What-If plan that models a few extra years of work so they can compare scenarios.

The Base Plan

Retiring at Age 61

Eve and Owen create a Base Plan that includes Eve's pension, their salaries, and a $6,000 annual retirement contribution from their employers. They set the model so that each begin Social Security at their full retirement age of 67.

They run a report and MaxiFi discovers their annual discretionary spending. Discretionary spending is the inflation-adjusted amount left over to spend each year after paying fixed expenses like taxes, housing costs, and Medicare Plan B costs. MaxiFi creates a unique saving and withdraw pattern from their non-retirement assets (i.e., from their pool of $100,000 in regular assets) that keeps this discretionary spending smooth from year to year even though fixed spending changes. Their sources of income include Social Security benefits, withdraws from retirement accounts, Eve's pension, and some earnings each year in their taxable and qualified retirement accounts.

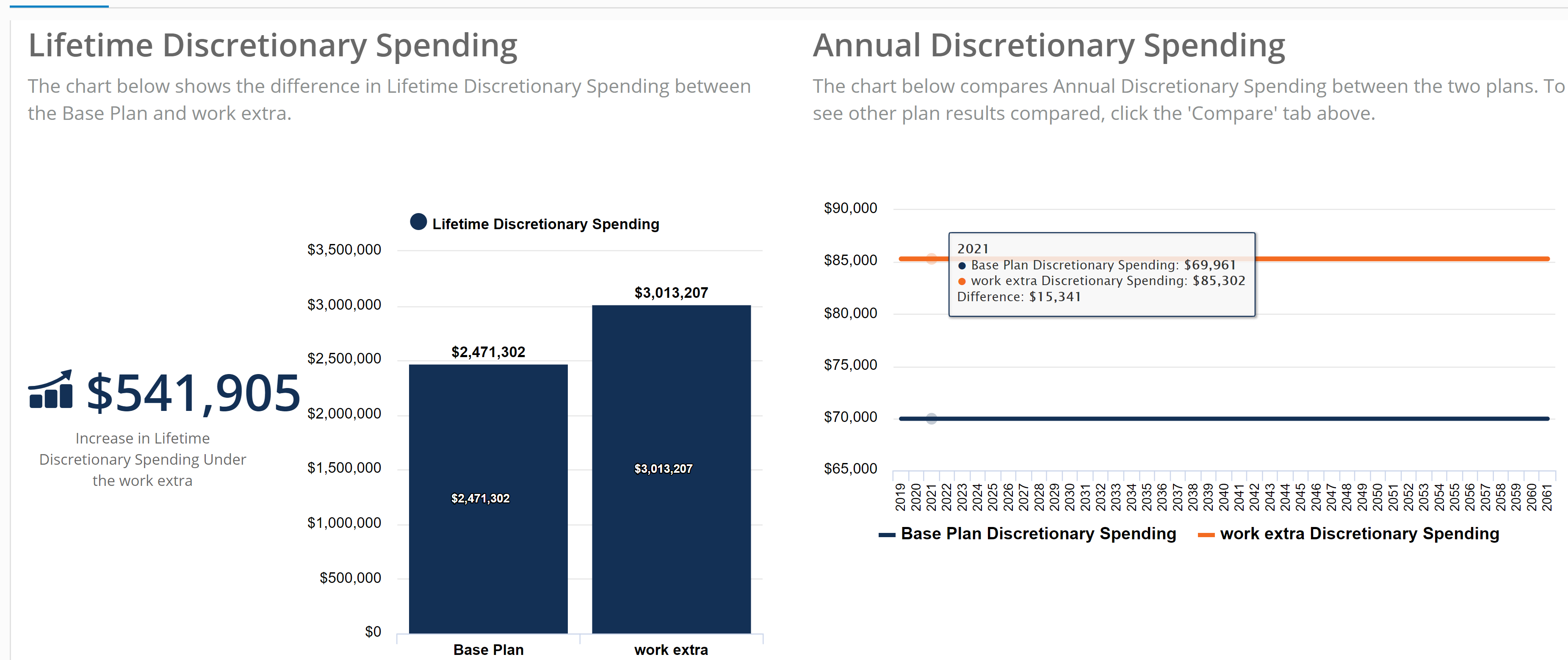

What they learn, the bottom line, is that they can spend an inflation-adjusted $69,961 each year after fixed expenses (taxes, housing, Medicare B, and their health insurance through age 64).

How Much is Enough?

So is a combined saving of $500,000 in the 401K enough to retire on? The answer of course all depends on how Eve and Owen feel about living on $69,961 of inflation-adjusted spending each year from their current age, 58, through 100. Were they to tally from recent years their annual after-tax, after-housing discretionary spending and discover that they routinely spend say $60,000 each year, well, then maybe the extra spending cushion the models describes makes them confident enough to retire at 61 as the model shows. Some people would certainly think so. They feel they could do it but they also wonder how this model changes if they work a few more years.

What if we retire at age 65 instead?

Work through age 64

If they run the program again but this time indicate that they are willing to wait until age 65 to retire, they learn they can have $85,302 in discretionary spending. That's $15,341 more to spend each year compared to the base model for the rest of their lives. This improved living standard is the result of more labor earnings of course (which may mean higher Social Security benefits), but also a combined $12,000 each year of employer contributions for a few more years and no extra costs for health insurance before age 65 since they are currently covered by their employer's plan.

How Much is Enough and is the Plan Realistic?

Granted, the case described above is a simple model for the purpose of illustration. They might want to add long term care expenses, or they might have an inheritance. They might want extra money for expensive vacations, or they might downsize their home. The main point, however, is that MaxiFi Planner doesn't require them to rely on general rules of thumb about retirement saving or crude calculations. With any scenario they are able to remove the mystery and discover their annual discretionary spending (a very concrete and meaningful number to evaluate) and decide for themselves how to answer the question: Do we have enough to retire?